Crypto has never been more front and center than it is in 2025. Ever since Donald Trump stepped back into the White House, Wall Street’s been glued to Bitcoin’s price just as much as it watches Tesla, Nvidia, or the S&P 500.

But while flashy tokens and meme coins steal the headlines, a quieter crypto revolution is unfolding and it’s led by stablecoins.

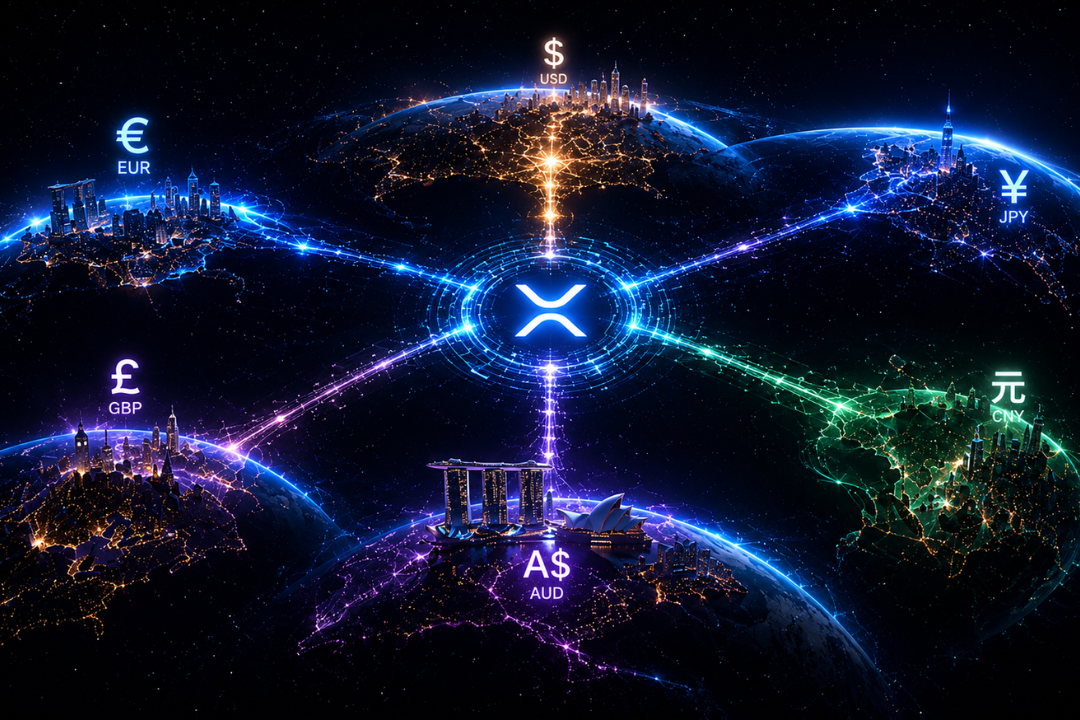

Once relegated to the shadows, stablecoins have emerged as one of the most practical pieces of the crypto puzzle. Unlike volatile coins like Bitcoin, stablecoins are pegged to traditional currencies like the U.S. dollar or euro, which means they can serve all the functions of regular money.

They’re becoming crucial tools for everything from bank-to-bank transfers to sending remittances overseas. Stablecoins may not have the meme magic or speculative hype of other cryptos, but they’re the bridge between the digital and traditional financial worlds.

In 2024 alone, global stablecoin transactions topped a whopping $27.6 trillion. Today, in 2025, stablecoins boast a market capitalization of $238 billion and most of this growth has quietly flown under the radar.

Banks and Governments Catch Up

So why the sudden surge in demand? Partly because the world’s biggest banks are all aboard. Back in 2019, JP Morgan launched the JPM Coin for internal transfers. Now, interbank transactions powered by stablecoins have exploded, hitting $1 billion daily. That kind of money movement forced governments to step in and create rules.

In Europe, regulators moved fast. The European Union’s Markets in Crypto-Assets Regulation (MiCA) took full effect at the end of 2024, offering clear rules aimed at protecting consumers and preventing money laundering. Thanks to MiCA, stablecoins have seeped into daily European life almost unnoticed like a wolf in sheep’s clothing.

Trust and transparency have been crucial to MiCA’s rollout, overseen by the European Banking Authority. The result? Transactions in EURC, a euro-pegged stablecoin, shot up from $7 million in December to $21 million in January 2025. It’s clear everyday Europeans want stablecoins, especially for cross-border payments and remittances in a world where migration and open borders keep growing in importance.

A New Era for Stablecoins in the U.S.

Across the Atlantic, the U.S. has had a rockier relationship with crypto. Although JP Morgan was an early pioneer in cross-bank stablecoin payments, crypto faced stiff resistance under SEC Chairman Gary Gensler. He famously claimed crypto was “unlikely [to] be a currency,” arguing that many leaders in the space were “either in jail or awaiting extradition.”

Crypto struggled for acceptance until Donald Trump returned to office. Since then, regulation in the U.S. has shifted at lightning speed, especially with the introduction of the GENIUS Act.

Officially known as the Guiding and Establishing National Innovation for U.S. Stablecoins Act, this law finally gives both stablecoin issuers and users clarity on where they stand legally. It also designates the Commodity Futures Trading Commission (CFTC) as the main regulator for digital commodities and payment stablecoins, giving stablecoins a firmer seat in traditional finance.

Though the U.S. stablecoin market still lags behind Europe’s in some respects, the global ripple effect of U.S. regulation can’t be overstated. As the article puts it: “If the world salutes the euro, it bows to the dollar,” and stablecoins are shaping up to be another powerful tool in America’s financial arsenal.

Standard Chartered, one of the UK’s biggest banks, predicts the GENIUS Act could catapult the stablecoin market from $230 billion today to $2 trillion by the end of 2028.

A Seat at the TradFi Table

Perhaps one of the most staggering signs of how deeply stablecoins are infiltrating traditional finance is the U.S. Treasury market. By 2030, stablecoin issuers like Tether and Circle are expected to buy $1.2 trillion in U.S. debt. That’s more than the treasury holdings of major nations like China, Japan, or the UK a monumental shift that would have seemed unthinkable a few years ago.

With both the GENIUS Act and MiCA now in full swing, stablecoin use at both institutional and consumer levels is poised to surge. Mastercard’s Vice President of blockchain and digital assets, Raj Dhamodharan, recently put it best:

“Most people won’t even know they’re using stablecoins.”

The infrastructure for digital payments is already here. Soon, the money we see in our bank apps could be backed by a digital dollar or euro without most of us ever noticing.

It might sound futuristic, but in reality, banking is simply catching up to what consumers want: faster, cheaper, borderless transactions. This revolution may be quiet, but its impact in the years ahead will be impossible to ignore.